My goal with Blocksplain is to track blockchain and cryptocurrency startups, which some are calling “Web 3” companies, and explain how they fit into the emerging blockchain ecosystem. But in order to understand the potential value of these startups, we first need to understand how the ecosystem itself is progressing. That’s my aim in this series of posts entitled Infrastructure Trends.

Chief among the infrastructure needs of blockchain startups is, of course, the blockchain itself. Most of these new companies will use a public blockchain, and most will choose one of the two biggest: Bitcoin or Ethereum. In this first post of the series, I’ll examine the size of these blockchains and what issues (if any) that’s causing.

A very quick explanation of what a blockchain is. Simply put, it’s a distributed database. Don and Alex Tapscott defined it well in their book Blockchain Revolution: “the blockchain is an incorruptible digital ledger of economic transactions that can be programmed to record not just financial transactions but virtually everything of value.”

That word “incorruptible” is key. It means that every single transaction in a public blockchain, from the very first block to the very latest, has to be verified by each distributed node. That means there are now hundreds of gigabytes of blockchain data clogging up computers across the globe.

Growth of blockchains

Bitcoin’s blockchain began in January 2009, when the mysterious Satoshi Nakamoto mined the first block of bitcoins (known as the “genesis block”). Ethereum’s blockchain started in July 2015, when its genesis block was made available.

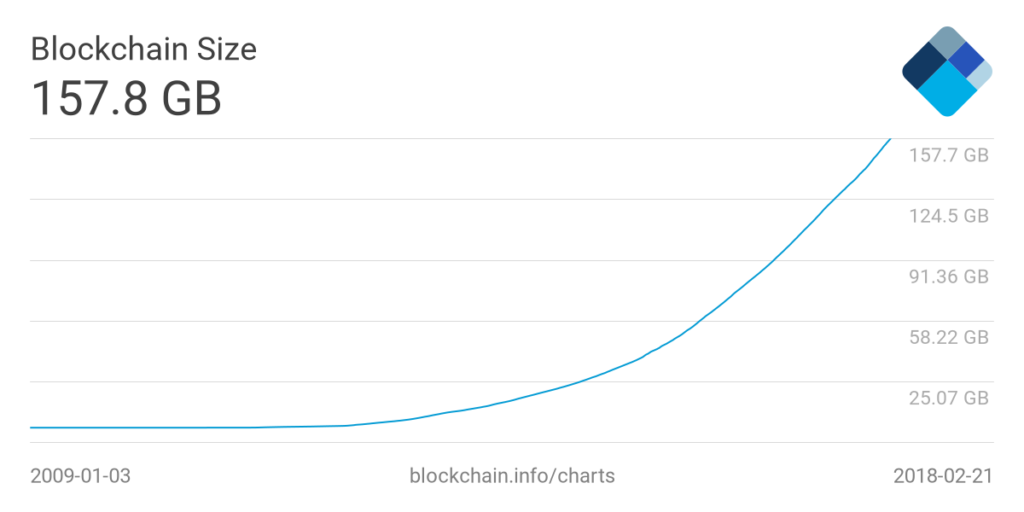

If you become a full node for the Bitcoin blockchain, meaning you help validate ongoing transactions, you basically have to download the entire database first. According to Blockchain.info, the Bitcoin blockchain was 149 GB at the end of 2017. It’s 157.8 GB at time of writing. This represents “the total size of all block headers and transactions.”

As you can see in the above chart, Bitcoin’s blockchain is growing at a stable, linear rate.

It isn’t quite so simple with the Ethereum blockchain. Bitcoin investor Alistair Milne caused some controversy recently when he posted this tweet:

Ethereum's blockchain is now >3x the size of Bitcoin's pic.twitter.com/c4c9mfu6qi

— Alistair Milne (@alistairmilne) February 12, 2018

What Milne neglected to mention is that there’s a concept in Ethereum called “pruning” – which means you don’t need to download the entire blockchain to be a full node. It’s horrendously complex, as this explanation details.

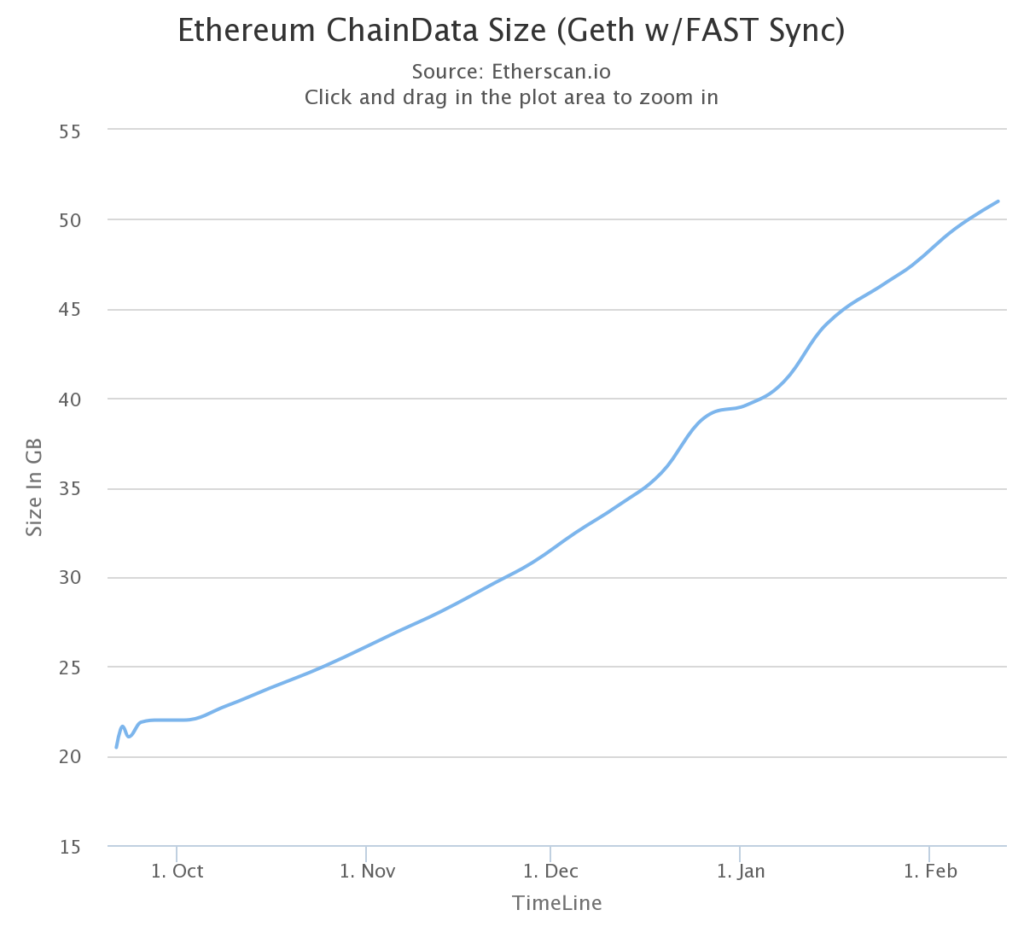

Basically if you use the “fast sync” mode on the Geth client, the blockchain size is closer to 50 GB according to Etherscan:

On the Parity client, which has a “warp” download speed, the size is even lower.

Impact on blockchain startups

What does all this mean to blockchain startups who are building on top of Bitcoin and Ethereum?

Arguably Bitcoin’s blockchain size is more dependable because it’s growing at a stable, linear rate. Ethereum’s blockchain is more complex and hence less stable.

However the ability to “prune” the Ethereum blockchain and still be a full node seems like a useful innovation. My understanding is that while you can prune the Bitcoin blockchain too, you cannot then remain a full node.

How important is the size of the blockchain to startups? Well as long as the Bitcoin and Ethereum nodes continue to validate all transactions and keep growing the blockchain, it’s not something startups need to worry too much about.

Of more concern to startups is the speed of transactions, which we’ll look at next in the Blocksplain Infrastructure Trends series.

More in this series: Infrastructure trends part 2: transaction speeds